Bank of Canada holds overnight rate at 1.75%

Martin Jensen • July 11, 2019

Bank of Canada Maintains Overnight Rate and Raises 2019 Forecast

The Bank of Canada held the target overnight rate at 1.75% for the sixth consecutive decision and showed little willingness to ease monetary policy, as stronger domestic growth offsets the risk of mounting global trade tensions. There has been ongoing speculation that the Bank of Canada would be pushed into cutting interest rates by the Fed. I do not believe the Bank will let the US dictate monetary policy when the Canadian economy is clearly on the mend. To be sure, trade tensions have slowed the global economic outlook, especially in curbing manufacturing activity, business investment, and lowering commodity prices. But the Bank as already incorporated these effects in previous Monetary Policy Reports (MPR) and today's forecast has made further adjustments in light of weaker sentiment and activity in other major economies.

The Governing Council stated in today's press release that central banks in the US and Europe have signalled their readiness to cut interest rates and further policy stimulus has been implemented in China. Thus, global financial conditions have eased substantially. The Bank now expects global GDP to grow by 3% in 2019 and to strengthen to 3.25% in 2020 and 2021, with the US slowing to a pace near its potential of around 2%. Escalation of trade tensions remains the most significant downside risk to the global and Canadian outlooks.

The Bank of Canada released the July MPR today, showing that following temporary weakness in late 2018 and early 2019, Canada's economy is returning to growth around potential, as they have expected. Growth in the second quarter is stronger than earlier predicted, mostly due to some temporary factors, including the reversal of weather-related slowdowns in the first quarter and a surge in oil production. Consumption has strengthened, supported by a healthy labour market. At the national level, the housing market is stabilizing, although there remain significant adjustments underway in BC. A meaningful decline in longer-term mortgage rates is supporting housing activity. The Bank now expects real GDP growth to average 1.3% in 2019 and about 2% in 2020 and 2021.

Inflation remains at roughly the 2% target, with some upward pressure from higher food and auto prices. Core measures of inflation are also close to 2%. CPI inflation will likely dip this year because of the dynamics of gasoline prices and some other temporary factors. As slack in the economy is absorbed, and these temporary effects wane, inflation is expected to return sustainably to 2% by mid-2020.

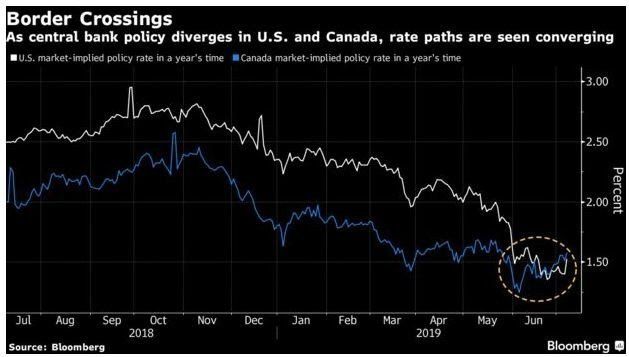

Bottom Line: The Canadian economy is returning to potential growth. "As the Governing Council continues to monitor incoming data, it will pay particular attention to developments in the energy sector and the impact of trade conflicts on the prospects for Canadian growth and inflation." With this statement, Governor Poloz puts Canadian rates firmly on hold as Fed Chair Jerome Powell signals openness to a rate cut as uncertainty dims the US outlook.

The Canadian central bank is in no hurry to move interest rates in either direction and has signalled it will remain on hold indefinitely, barring an unexpected exogenous shock.

This article was written by Dr. Sherry Cooper, DLCs Chief Economist, it was originally shared on her newsletter.

RECENT POSTS

When you’re buying a home, two terms often cause confusion: deposit and down payment . While they’re related, they serve very different purposes in the homebuying process. Here’s what you need to know. What Is a Deposit? A deposit is the money you provide when you make an offer on a property. Think of it as a show of good faith that proves you’re serious about purchasing. How it works : Typically, you provide a certified cheque or bank draft that your real estate brokerage holds in trust. If your offer is accepted, the deposit remains in trust until the deal moves forward. If negotiations fall through, the deposit is refunded. Connection to your down payment : Once the sale is finalized, your deposit becomes part of your total down payment. Why it matters : The amount is negotiable, but a larger deposit can make your offer more attractive in a competitive market. Keep in mind, however, that if you back out after conditions are removed, you risk losing your deposit. What Is a Down Payment? Your down payment is the amount you contribute toward the purchase price of your home when securing a mortgage. Minimum requirement : In Canada, the minimum down payment is 5% of the home’s purchase price. Anything less than 20% requires mortgage default insurance. Sources : Down payments can come from your savings, the sale of another property, RRSP withdrawals (through the Home Buyers’ Plan), a gift from family, or even borrowed funds. Example: How They Work Together Imagine you’re buying a $400,000 home with a 10% down payment ($40,000). When you make your offer, you provide a $10,000 deposit . Once conditions are met, that deposit is transferred to your lawyer’s trust account. At closing, you add the remaining $30,000 to complete your full down payment. The lender provides the rest—$360,000—through your mortgage. The Bottom Line Your deposit shows commitment and secures your offer, while your down payment is what makes the mortgage possible. Together, they work hand in hand to get you into your new home. 📞 If you’d like clarity on deposits, down payments, or any other part of the mortgage process, let’s connect. I’d be happy to walk you through it step by step.

Don’t Forget About Closing Costs When planning to buy a home, most people focus on saving for the down payment. But the truth is, that’s only part of the equation. To actually finalize the purchase, you’ll also need to budget for closing costs —the out-of-pocket expenses that come up before you get the keys. Closing costs can add up quickly, which is why they should be part of your pre-approval conversation right from the start. Lenders will even require proof that you’ve got enough funds set aside. For example, if you’re getting an insured (high-ratio) mortgage, you’ll need at least 1.5% of the purchase price available in addition to your down payment. That means a 10% down payment actually requires 11.5% of the purchase price in cash to make everything work. Let’s break down some of the most common expenses you should prepare for: 1. Home Inspection & Appraisal Inspection : Paid by you, this gives peace of mind that the property is in good shape and doesn’t have hidden problems. Appraisal : Required by the lender to confirm value. Sometimes this is covered by mortgage insurance, sometimes by you. 2. Legal Fees A lawyer or notary is required to handle the title transfer and make sure the mortgage is properly registered. Legal fees are often one of the larger closing costs—unless you’re also responsible for property transfer tax. 3. Taxes Many provinces charge a property or land transfer tax based on the home’s purchase price. These fees can range from hundreds to thousands of dollars, so you’ll want to factor them in early. 4. Insurance Property insurance is mandatory—lenders won’t release funds without proof that the home is insured on closing day. Optional coverage like mortgage life, disability, or critical illness insurance may also be worth considering depending on your financial plan. 5. Moving Costs Whether you’re renting a truck, hiring movers, or bribing friends with pizza and gas money, moving comes with expenses. Cross-country moves especially can be surprisingly pricey. 6. Utilities & Deposits Setting up new services (electricity, water, internet) can involve connection fees or deposits, particularly if you don’t already have a payment history with the utility provider. Plan Ahead, Stress Less This list covers the big-ticket items, but every purchase is unique. That’s why it pays to have an accurate estimate of your personal closing costs before you make an offer. If you’d like help planning ahead—or want a breakdown tailored to your situation—let’s connect. I’d be happy to walk you through the numbers and make sure you’re fully prepared.

Why a Mortgage Pre-Approval Protects Both Your Head and Your Heart There’s no denying it—buying a home is an emotional journey. In a competitive market, it can feel like you need to stretch beyond your comfort zone or bid above asking just to have a chance. That pressure can make it hard to separate what you want from what you can realistically afford. One of the biggest pitfalls buyers face is falling in love with a home that’s outside their price range. Once that happens, every other property seems like a compromise—even the ones that might have been a perfect fit otherwise. The best way to avoid this heartache? Get pre-approved before you start shopping. What a Pre-Approval Does for You A mortgage pre-approval gives you more than just a number—it provides clarity, confidence, and protection: Know your buying power : Shop within your true price range and avoid disappointment. Spot potential roadblocks : Uncover issues like credit bureau errors before you make an offer. Get organized : Learn exactly what documentation you’ll need so there are no surprises. Lock in a rate : Many lenders hold your rate for 30–120 days, giving you peace of mind if rates rise. Save yourself heartache : Protect yourself from falling for a home you can’t afford. Head vs. Heart Buying a home is about balance. Your head tells you what’s financially sound, your heart tells you what feels right—and both matter. A pre-approval helps bring those two sides together, so you can make confident choices without emotional stress clouding your judgment. The Bottom Line Looking at properties for fun is one thing—but if you’re serious about buying, a pre-approval is the smartest first step you can take. It sets realistic expectations, saves time, and protects your emotions along the way. If you’d like to explore your options and get pre-approved, I’d be happy to walk through the process with you. Let’s make sure you’re ready to shop with confidence.