Bank of Canada Hikes Rates

Bank of Canada Turns the Tide

For the first time in seven years , the Bank of Canada announced today that it was hiking its key overnight rate by a quarter percentage point (25 basis points) bringing it to 0.75 percent as the economy has staged a broadly based economic expansion this year. In a break from tradition, the Bank has taken this action even though inflation remains well below its target rate of 2 percent. Indeed, inflation has hit its lowest level since 1999. The consumer price index (CPI), released in late June, rose only 1.3 percent in May from a year ago, down from an annual pace of 1.6 percent in April. Both Governor Poloz and Senior Deputy Governor Wilkins have emphasized that the Bank must begin to hike rates pre-emptively due to the lagged effect of monetary tightening.

Measures of annual core inflation, a key indicator tracked by the Bank of Canada, which excludes volatile components such as food and energy, fell to its lowest in almost two decades. The average of the central bank’s three core measures declined to 1.3 percent, its lowest level since March 1999. The Bank has recently played down sluggish inflation numbers, suggesting they reflect the lagged effects of past excess capacity. Incoming inflation figures have been well below the Bank's forecasts and will likely remain low for some time as oil prices are wobbling downward and wage inflation is a mere 1.3 percent--just keeping up with core inflation.

Last Friday's continued strong employment report for June cinched the rate-hike. Employment rose a hefty 45,300, lifting the 12-month gain to a whopping 350,000 and trimming the jobless rate to match the cycle low of 6.5%. What's more, total hours worked surged in the second quarter at the fastest rate since 2003. GDP climbed an impressive 3.3% year-over-year in April, while record levels of exports and imports suggest activity stayed on track in May, and further record highs for auto sales suggest consumers kept right on spending in June. Spending strength is yet another sign that after two years of lagging behind, Canada’s overall growth rate has come bouncing back in the past year to surpass the U.S. pace. The Bank now expects the output gap to close around year end.

Markets have been expecting this move for some time, as monetary policymakers have publicly stated that the 2015 interest-rate cuts appear to have done their job. Governor Stephen Poloz has said that the Canadian economy enjoyed "surprisingly" strong growth in the first three months of this year and that he expects the growth pace to remain above potential (estimated at 1-3/4 percent), setting the stage for this rate hike. In response, Canadian bond yields have moved higher, the Canadian dollar has surged anew, and the big Canadian banks raised mortgage rates by roughly 20 basis points last week in anticipation of this move. The 5-year Government of Canada bond yield has surged nearly 50 basis points in the past month. Indeed, 10-year government yields are up to roughly 1.9 percent, their highest yield in more than two years. The Canadian dollar surged to above 77.5 cents, the strongest level in 10 months , up more than 6 percent from the lows in early May. Stalling oil prices may reverse some of the loonie's recent gain.

The big banks will also raise their prime rates, driving up the cost of variable rate mortgages, other loans and lines of credit tied to the benchmark rate. While the banks shaved their response to the interest rate cuts to less than the 25 basis points decline when monetary policy was easing, it is likely now that banks will adjust lending rates to close to the full 25 basis point increase. This asymmetric response is consistent with the desire of regulators to slow the growth in household debt.

Housing is one crucial component of the Canadian economy, and it has slowed meaningfully at the national level, in line with the central bank's expectations. Prices and sales have declined in the Greater Toronto Area and surrounding municipalities since the Ontario Fair Housing Plan announcement in late April. However, housing activity has gained momentum in Montreal and Ottawa, while Alberta stabilizes and Vancouver posted a modest bounceback from the swoon following its August 2016 imposition of a foreign buyers' tax. The underlying strength in many housing markets is the reason why policymakers are proposing new rules to tighten mortgage lending. This time OSFI--the regulator of financial institutions--is proposing that banks stress test non-insured borrowers at two percentage points above the contract rate. This despite the fact that non-insured borrowers are putting at least 20 percent down on their home purchase. A small BoC rate hike would reinforce the multi-faceted steps to calm the broader housing market.

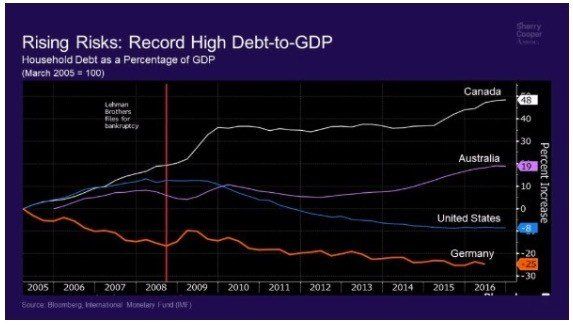

The Bank has repeatedly stated that "macroprudential and other policy measures have contributed to more sustainable debt profiles," even though household debt-to-income levels have hit a record high (see chart).

Uncertainties, of course, persist--particularly on the trade side as NAFTA is renegotiated in fewer than 90 days. The U.S. has already imposed duties on softwood lumber, and President Trump's rhetoric remains hostile, threatening U.S. import duties on steel and other products. These uncertainties notwithstanding, I expect another Bank of Canada rate hike in the fourth quarter. The Federal Reserve will also likely increase rates in Q4. Look for a slow crawl upward in interest rates from both central banks in 2018.

by Dr. Sherry Cooper.

Bank of Canada Rate Announcement July 12th, 2017

The following is the latest Bank of Canada rate announcement, if you have any questions about what this rate increase means for you and your mortgage, please don't hesitate to contact me anytime. If you're a fixed rate mortgage holder, this change doesn't impact you, however if you are a variable rate mortgage holder, you can expect bank prime to be going up at the beginning of next month.

Bank of Canada increases overnight rate target to 3/4 per cent

The Bank of Canada is raising its target for the overnight rate to 3/4 per cent. The Bank Rate is correspondingly 1 per cent and the deposit rate is 1/2 per cent. Recent data have bolstered the Bank’s confidence in its outlook for above-potential growth and the absorption of excess capacity in the economy. The Bank acknowledges recent softness in inflation but judges this to be temporary. Recognizing the lag between monetary policy actions and future inflation, Governing Council considers it appropriate to raise its overnight rate target at this time.

The global economy continues to strengthen and growth is broadening across countries and regions. The US economy was tepid in the first quarter of 2017 but is now growing at a solid pace, underpinned by a robust labour market and stronger investment. Above-potential growth is becoming more widespread in the euro area. However, elevated geopolitical uncertainty still clouds the global outlook, particularly for trade and investment. Meanwhile, world oil prices have softened as markets work toward a new supply/demand balance.

Canada’s economy has been robust, fuelled by household spending. As a result, a significant amount of economic slack has been absorbed. The very strong growth of the first quarter is expected to moderate over the balance of the year, but remain above potential. Growth is broadening across industries and regions and therefore becoming more sustainable. As the adjustment to lower oil prices is largely complete, both the goods and services sectors are expanding. Household spending will likely remain solid in the months ahead, supported by rising employment and wages, but its pace is expected to slow over the projection horizon. At the same time, exports should make an increasing contribution to GDP growth. Business investment should also add to growth, a view supported by the most recent Business Outlook Survey.

The Bank estimates real GDP growth will moderate further over the projection horizon, from 2.8 per cent in 2017 to 2.0 per cent in 2018 and 1.6 per cent in 2019. The output gap is now projected to close around the end of 2017, earlier than the Bank anticipated in its April Monetary Policy Report (MPR).

CPI inflation has eased in recent months and the Bank’s three measures of core inflation all remain below 2 per cent. The factors behind soft inflation appear to be mostly temporary, including heightened food price competition, electricity rebates in Ontario, and changes in automobile pricing. As the effects of these relative price movements fade and excess capacity is absorbed, the Bank expects inflation to return to close to 2 per cent by the middle of 2018. The Bank will continue to analyze short-term inflation fluctuations to determine the extent to which it remains appropriate to look through them.

Governing Council judges that the current outlook warrants today’s withdrawal of some of the monetary policy stimulus in the economy. Future adjustments to the target for the overnight rate will be guided by incoming data as they inform the Bank’s inflation outlook, keeping in mind continued uncertainty and financial system vulnerabilities.

Here are the announcements dates set out for the remainder of 2017.

- Wednesday 6 September

- Wednesday 25 October*

- Wednesday 6 December

*Monetary Policy Report published

All rate announcements will be made at 10:00 (ET), and the Monetary Policy Report will continue to be published concurrently with the January, April, July and October rate announcements.

Monetary Policy Report July 2017